At the end of 2017, Congress enacted sweeping tax reform that has widespread effects on both individual physicians and medical practices.

This is the largest change to the Tax Code in years, with many changes taking effect January 1, 2018. This article provides an overview of some of the changes that we felt would have the most impact on physicians and their practices.

Taxes at the Individual Level

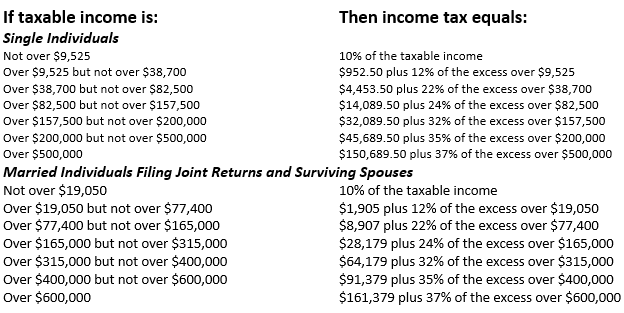

For individuals, first and foremost are changes to the seven tax rates and brackets, now with a top rate of 37 percent:

Capital gains and dividend rates remain unchanged.

In addition to rate and bracket changes, there are several other aspects to the new law affecting individuals. The standard deduction has nearly doubled, from what would have been $6,500 in 2018 for single taxpayers and $13,000 for married taxpayers filing jointly to $12,000 and $24,000 respectively. However, there will no longer be a deduction for personal or dependency exemptions. These had previously been reduced or eliminated for many high-income taxpayers.

While the Alternative Minimum Tax (AMT) was not repealed for individuals, the exemption amounts increased to $70,300 for single taxpayers and $109,400 for married filing jointly, and the exemption phase-out now will not begin until $500,000 for single taxpayers and $1,000,000 for married filers.

The “kiddie” tax has been simplified, and unearned income of children to whom this applies will now be taxed at trust and estate rates rather than at their parents’ rates. This also means there will no longer be a need to include siblings’ unearned income when calculating the tax. Also notable for parents, Section 529 plan distributions of up to $10,000 per year per student can be used for elementary and secondary school expenses under the new law. Previously, such distributions could only be used for qualified higher education expenses. The child tax credit increases to $2,000 per child with $1,400 of that being refundable under the new law.

Many changes to itemized deductions for individual taxpayers may impact many physicians in significant ways. The deduction for state and local income, sales and property taxes is capped at $10,000 for married and single taxpayers and $5,000 for head of household filers. Most miscellaneous itemized deductions are eliminated, including tax preparation fees, investment fees, and unreimbursed employee business expenses. The medical expense deduction floor is reduced to 7.5 percent for 2017 and 2018.

For mortgages incurred after December 16, 2017, interest is deductible for the principal residence and a second residence on loan principal of $750,000 (previously the loan limitation was $1,000,000). Current mortgages are grandfathered at the $1 million amount. Refinancing of grandfathered mortgages is also grandfathered but not beyond the term and amount of the original mortgage. In addition, interest on home equity loans will no longer be deductible.

The limit for charitable contributions to public charities increases to 60 percent of AGI from the previous 50 percent, however the deduction for contributions made in exchange for college athletic event seating rights is no longer allowed. The new law also eliminates PEASE limitations, which reduced itemized deductions for higher income taxpayers.

The estate tax exemption and gift tax exemption are generally doubled from $5 million per individual to $10 million as indexed for inflation occurring after 2011 for decedents dying after December 31, 2017 and before January 1, 2026. For 2018, the exclusion amount is $11.2 million.

Taxes at the Practice Level

Business taxpayers will also see many changes. Perhaps most notable is the new flat 21 percent corporate tax rate for corporation tax years beginning after December 31, 2017. Alternative minimum tax has been repealed for corporations. There is also a provision for immediate 100 percent expensing for the purchase of business equipment placed in service after September 27, 2017 and before January 1, 2023. The depreciation cap on luxury autos has been raised, and the limitation for Section 179 expensing has been set at $1 million. The deduction for net interest expenses will now be limited to 30 percent of adjusted taxable income. Net operating loss carryforwards will also be limited to 80 percent of taxable income, and Section 1031 like kind exchanges will be limited to real property. The deduction for any activity deemed entertainment, amusement or recreation (including club membership dues) has been repealed, but 50 percent of business meals will still be deductible.

In what may be the greatest failure of “tax simplification” there are new provisions for pass-through business income – including that from S corporations, partnerships and sole proprietorships – impacting most medical practices.

There will be a 20 percent deduction against qualified business income of these pass-through entities. The deduction amount will be the lesser of:

• 20 percent of the taxpayer’s qualified business income; or

• The greater of 1) 50 percent of W2 wages paid with respect to the business or 2) the sum of 25 percent of the W2 wages paid plus 2.5 percent of unadjusted basis of all qualified property

The deduction is further limited to the net of taxpayer’s taxable income less taxpayer’s net capital gain. The wage limitation does not apply to married taxpayers with taxable income under $315,000 ($157,500 for single taxpayers).

However, specified service businesses (accountants, attorneys, doctors, etc.) are excluded from the deduction unless they are under the $315,000 / $157,500 taxable income thresholds.

Conclusion

In our experience, the new tax law will mean lower taxes for some physicians and higher taxes for others. For all physicians, there is no year to be more focused on tax efficiency than 2018.

SPECIAL OFFERS: To receive free hardcopies of Wealth Management Made Simple and For Doctors Only: A Guide to Working Less and Building More, please call 877-656-4362. Visit www.ojmbookstore.com and enter promotional code ASCCOM02 for a free ebook download of these books for your Kindle or iPad.

David B. Mandell, JD, MBA, is an attorney, consultant and author of more than a dozen books for doctors, including For Doctors Only: A Guide to Working Less and Building More. He is a principal of the wealth management firm OJM Group www.ojmgroup.com, where Carole C. Foos, CPA is also a principal and lead tax advisor. They can be reached at 877-656-4362 or mandell@ojmgroup.com.

Disclosure:

OJM Group, LLC. (“OJM”) is an SEC registered investment adviser with its principal place of business in the State of Ohio. OJM and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisers by those states in which OJM maintains clients. OJM may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. For information pertaining to the registration status of OJM, please contact OJM or refer to the Investment Adviser Public Disclosure web site www.adviserinfo.sec.gov.

For additional information about OJM, including fees and services, send for our disclosure brochure as set forth on Form ADV using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

This article contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized legal or tax advice. There is no guarantee that the views and opinions expressed in this article will be appropriate for your particular circumstances. Tax law changes frequently, accordingly information presented herein is subject to change without notice. You should seek professional tax and legal advice before implementing any strategy discussed herein.